D4 RINs explode higher as 45z status remains unclear

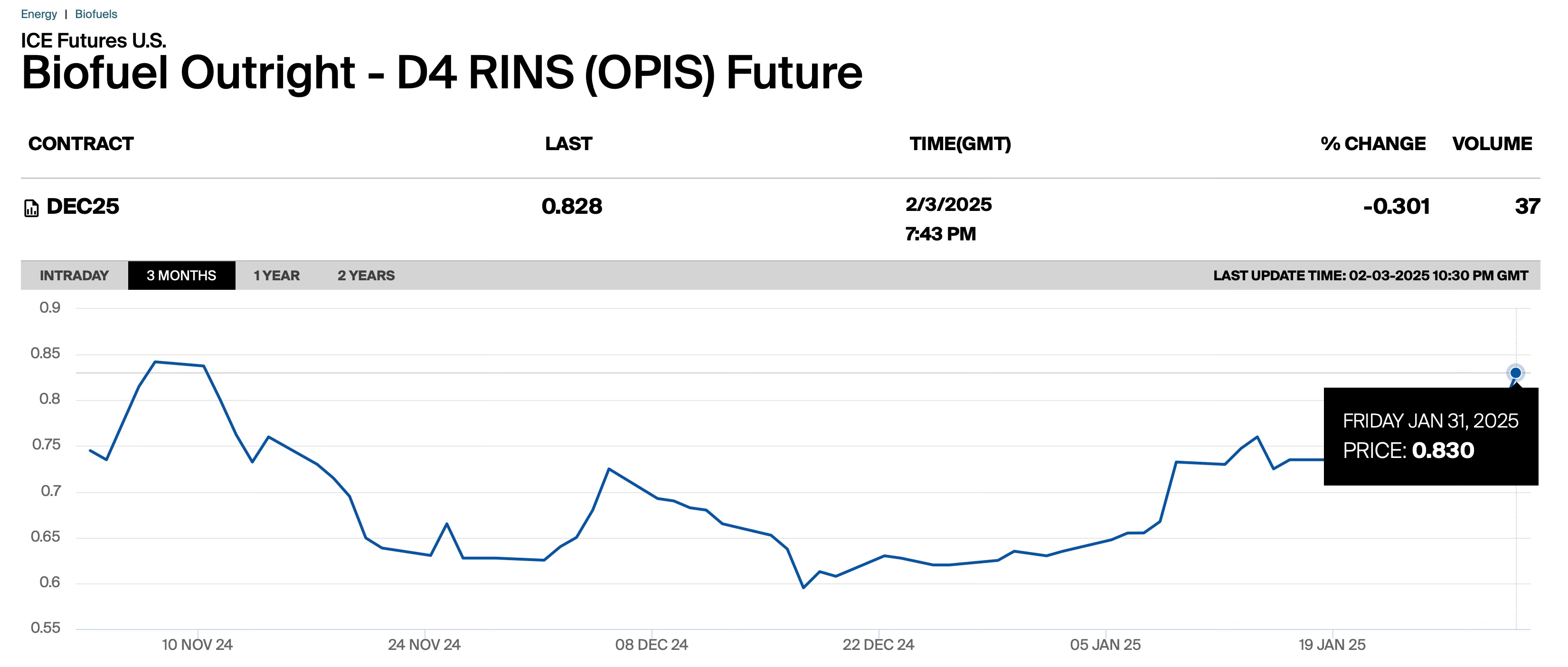

The U.S. renewable fuel credit markets experienced a dramatic move this week as D4 biomass-based diesel RINs surged to 83 cents per gallon, reflecting profound changes rippling through the biofuels industry. This price action comes as the market grapples with the transition from the expired $1/gallon blenders tax credit to the new uncertain carbon intensity-based 45Z credit system. Under the new framework, credits vary significantly based on feedstock type - from zero to around 16 cents for soybean oil depending on operations and 50-60 cents for waste oils. This structural shift is forcing a fundamental reassessment for most production economics across the sector and particularly conventional biodiesel plants. My assessment is we are going to lose 500Kt to 1 mil MT per month of Biodiesel production/feedstock demand if current situation remains.

The European market is simultaneously undergoing its own transformation as mandates tighten and demand patterns evolve. According to Valero's recent earnings call, their new Sustainable Aviation Fuel (SAF) facility is now fully operational, with initial production focused on European markets where mandates are driving demand. Current European market pricing shows Hydrotreated Vegetable Oil (HVO) trading at almost $100/mt above SAF levels, highlighting the complex optimization decisions producers face. The implementation of a 2% SAF mandate in both the EU and UK is creating new demand vectors just as the global supply chain adapts to changing incentive structures. SAF pricing in ARAG is down almost $100/mt in one week!

Supply-side dynamics are rapidly shifting as less efficient production comes under pressure. Imports of biodiesel and renewable diesel into the U.S. are expected to decline sharply as foreign production using imported feedstocks no longer qualifies for 45Z credits. Market participants anticipate a significant reconciliation of production capacity, particularly among facilities relying on virgin vegetable oil feedstocks that receive minimal support under the new system. This is occurring against a backdrop of a tightening vegetable oil markets while world consumption of major vegetable oils forecast to rise by only 2.5 million tonnes this season versus 8.8 million tonnes in 2023/24.

The waste oil market is emerging as a critical battlefield. Premium Used Cooking Oil (UCO) prices have remained firm despite recent market volatility, reflecting its favored status under both U.S. and European regulatory frameworks. Major producers like Diamond Green Diesel in the US maintain significant advantages through their waste oil-focused platforms and ability to optimize production between various markets and products. UCOME in Europe is trading spot at $1430/mt or +715 above ICE gasoil reflecting $330/mt gross margin. However, the broader industry faces challenges as increased demand for waste oils collides with inherently limited supply growth potential domestically and now volatile emerging market forex rates on account of tariff threats that could take China Yuan (CNY) back to 7.33 where it was already on Jan 8 and perhaps much higher. Euro is already at near-parity with $ at 1.02 … with most feedstock imports into EU denominated in USD, this is only pushing more costs on producers.

Looking ahead, the first quarter of 2025 is shaping up as a crucial transition period as markets seek new equilibrium levels. RIN prices may need to move to $1 or more to incentivize sufficient production given lower tax credit values, particularly for virgin oil-based facilities. Soybean oil is now 1.5x gasoil (diesel) values and BOGO now trading at +320 while Biodiesel screen crush is still barely under negative 29 c/gallon negative (-$57.50/mt) while European FAME is trading at $1178/mt spot which is a gross margin of $117/mt and probably mostly negative net returns for most producers in Europe. The interplay between U.S. RIN markets and European compliance markets will likely intensify as producers optimize their production slate and destination markets - look for more HVO headed to Europe. While well-positioned waste oil processors should continue to thrive, the broader industry faces a period of significant adjustment as it adapts to this new regulatory reality of no BTC and 45z uncertainties. This evolution could drive further consolidation in the sector as scale and feedstock flexibility become increasingly critical success factors.