Tallow continues to lead in EIA feedstock mix for Biodiesel/RD

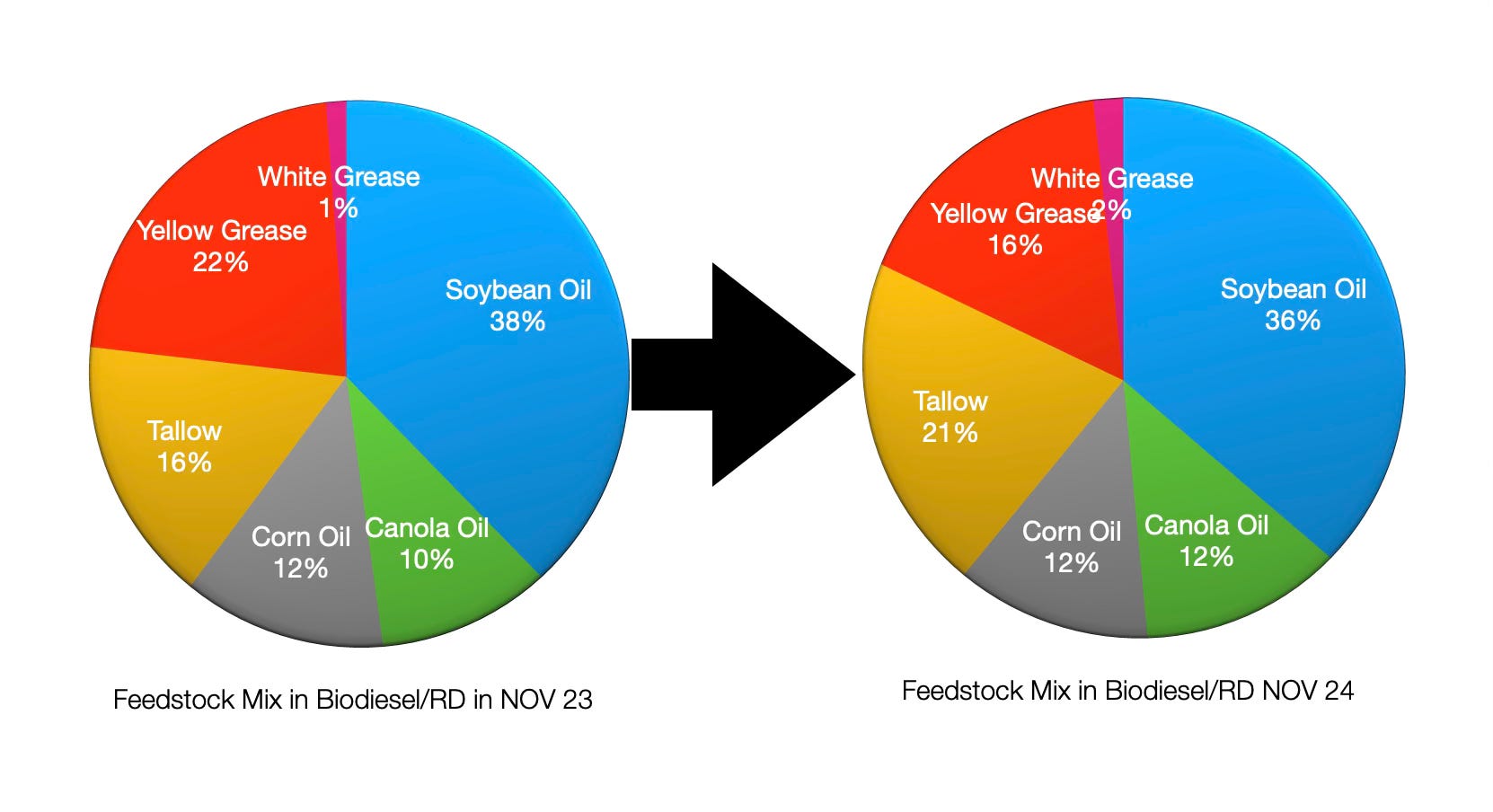

The November EIA feedstock data reveals a continuing shift in renewable fuel production patterns, with tallow emerging as a standout performer, surging nearly 50% year-over-year to 696 million pounds. This dramatic increase in tallow usage significantly outpaced other feedstock growth rates and reinforces its position as a crucial input for the renewable diesel and biodiesel sectors. Overall feedstock utilization showed an impressive 18.9% growth compared to November 2023, even as the industry navigates increasing regulatory uncertainty and new trade headwinds.

While soybean oil usage increased in absolute terms to 410 million pounds, its relative position in the feedstock slate continues to evolve as producers diversify their inputs. Canola oil consumption reached 404 million pounds, marking a 14.4% increase from November 2023. This uptick in canola usage follows a well-established seasonal pattern, though the recently announced tariffs on Canadian imports could significantly impact this traditional seasonal shift. Canola's superior cold-flow properties make it particularly valuable during winter months, but producers may need to seek alternative sources or adjust their strategies if Canadian supply chains face disruption from the new trade measures.

Yellow grease volumes saw a seasonal decline of 13.3% to 543 million pounds in November, compared to 626 million pounds in November 2023. This reduction follows expected seasonal variations, but the market is now closely watching how new tariffs on Mexican imports might affect cross-border waste oil trade flows. With tariffs being imposed on Canada, Mexico, and China simultaneously, the industry faces unprecedented challenges in international feedstock procurement. These trade measures are already strengthening the USD and creating additional headwinds for emerging markets, potentially reshaping traditional feedstock trade patterns.

The EIA data interpretation becomes even more complex given the current turmoil at the EPA, where internal tensions and staffing challenges are creating additional uncertainty for the biofuels industry. The implementation of new biofuel rules and potential changes to the 45Z credit program were already creating complexity in feedstock procurement strategies, but the reported internal struggles at EPA add another layer of uncertainty to the regulatory landscape. This regulatory ambiguity, combined with the new tariff regime, could significantly impact feedstock procurement strategies going forward.

The diversity in feedstock utilization, particularly the strong showing in tallow usage, demonstrates the industry's growing maturity and flexibility in managing its input slate. Total feedstock consumption growth of 18.9% year-over-year highlights the sector's robust expansion, even as it navigates seasonal shifts, regulatory uncertainties, and new trade barriers. The ability to pivot between feedstocks based on availability and operational requirements has become more crucial than ever. As we progress through 2025, this flexibility will be tested by the combined challenges of EPA regulatory uncertainty and the impact of new tariffs on international trade flows. The strengthening USD and pressure on emerging markets could create additional complications for global feedstock procurement, making domestic sources like tallow increasingly valuable to US producers.